Essay: On Black's Income Tax Cuts

The poor man's take on a rich man's plan

I am a bus driver. I am not an economist, not a financial analyst, not a policy researcher with letters after my name — except my CD issued after 15 years of service as a Maritime Warfare Officer in the RCN. What I am is a person who pays attention, who reads the public accounts, who has spent some evenings going through the actual numbers that governments publish and that most people never look at. I am not qualified to tell you what the textbooks say. I am qualified to tell you what the numbers say.

I want to be clear about that at the outset, because what follows is going to make Iain Black’s 20 percent personal income tax cut look like one of the most reckless fiscal proposals put forward by a BC Conservative leadership candidate in a generation. And if I can arrive at that conclusion sitting at a kitchen table with public documents and a calculator, imagine what a real economist does with it when Black is standing in front of cameras running for Premier. I am offering the rough draft. The professional demolition comes later.

So. What is Black proposing, and how has he defended it?

His five-point plan lists the 20 percent personal income tax cut as item one, described as a magnet for investment, a driver of job growth, and a tool for affordability. Every bracket. Every earner. Day one. His defence rests on three pillars: the economy grows when you cut taxes, the growth replaces much of the lost revenue, and the remainder can be covered by finding efficiencies — approximately three percent of government revenue, by his accounting. He has pointed to Gordon Campbell’s 2001 cuts as the historical proof of concept. What some might call basic economics.

I want to examine every one of those pillars. But first, the financial picture Black would be inheriting, a picture made significantly worse by eight years of reckless BC NDP fiscal management, and one that demands more discipline from its next steward, not less.

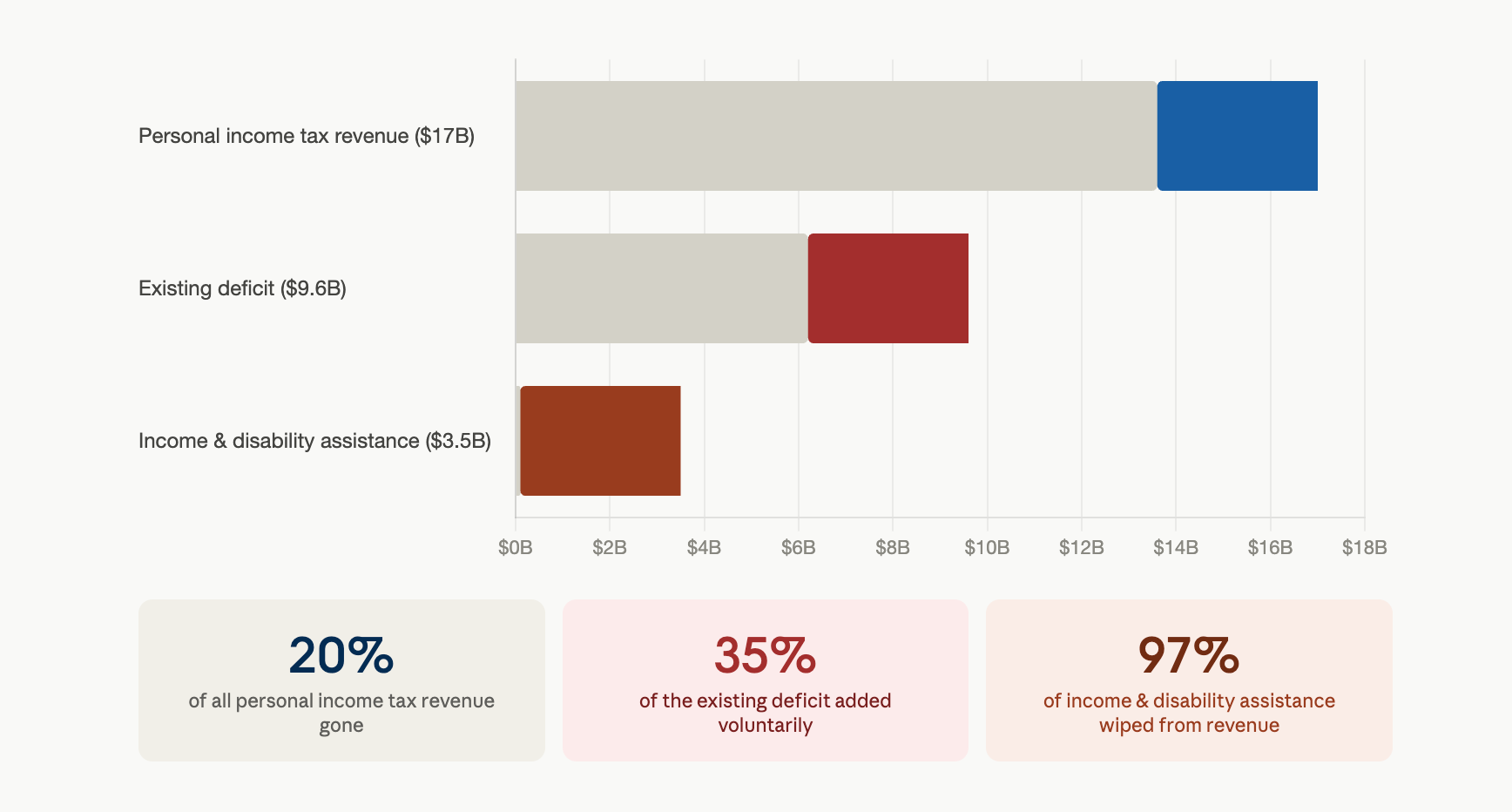

BC’s total consolidated revenue in 2024/25 came in at $84 billion. Of that, $49.4 billion was taxation. Personal income tax alone generated just over $17 billion. Corporate income tax contributed $8.3 billion. On the spending side, provincial operating expenses ran to $91.4 billion. The deficit for 2024/25 was $7.3 billion — lower than forecast, but still $7.3 billion more spent than collected. The current year deficit is projected at $9.6 billion. Next year’s is forecast at $13.3 billion — the largest in provincial history. Taxpayer-supported debt now sits at $99 billion and is projected to climb toward $189 billion over the next three fiscal years.

Servicing that debt already costs $4.4 billion per year. More than BC spends on child welfare. RBC projects debt-servicing costs rising from 4.3 cents per dollar of revenue today to 6.9 cents by 2027/28. TD Economics puts the outer-year interest bill at $8.7 billion annually — money that is gone before a single teacher is hired, a single hospital bed is funded, a single road is expanded or fixed.

This is the house Black wants to renovate by removing a load-bearing wall.

A 20 percent cut to personal income tax rates produces, arithmetically, a 20 percent reduction in personal income tax revenue. Against $17 billion in personal income tax receipts, that is a $3.4 billion reduction. Black calls it three percent of government revenue, which is only true if you use the full $84 billion consolidated figure as your denominator. Use total taxation revenue of $49.4 billion instead and it becomes 6.9 percent. The denominator he chose is the one that makes the number look smallest. Against the existing $9.6 billion deficit he would walk into on day one, it is an extra 35 percent of the shortfall he says he intends to shrink through economic growth. It is like digging an extra third deeper into a hole you promised to start filling.

And here is the comparison that stopped me cold when I worked it out.

BC spends approximately $3.5 billion per year providing income and disability assistance to roughly 253,000 British Columbians — people receiving financial support, transportation help, crisis supplements, and health supports. People who, without that program, have nowhere else to go. The revenue Black proposes to voluntarily surrender is essentially identical in size to what it costs to run that program entirely.

He is not proposing to eliminate income and disability assistance. No doubt he would insist on making that clear. But he is proposing to remove from the provincial treasury, permanently, on day one, a sum of money equal to what it costs to keep 253,000 of the most vulnerable people in this province from falling through the floor. He cannot do both things. He cannot cut $3.4 billion in annual revenue and protect every service that depends on it. One of those commitments is false. He has not told British Columbians which one.

Now let’s talk about who the cut actually benefits, because Black’s affordability framing needs stress-testing against the real numbers.

BC’s income tax runs seven brackets, from 5.06 percent on the first $49,000 of taxable income to 20.5 percent on income above $260,000. A flat 20 percent reduction in rates does not produce equal dollar benefits across earners. It produces benefits that scale with income, because the brackets are progressive and the cut is proportional and therefore regressive.

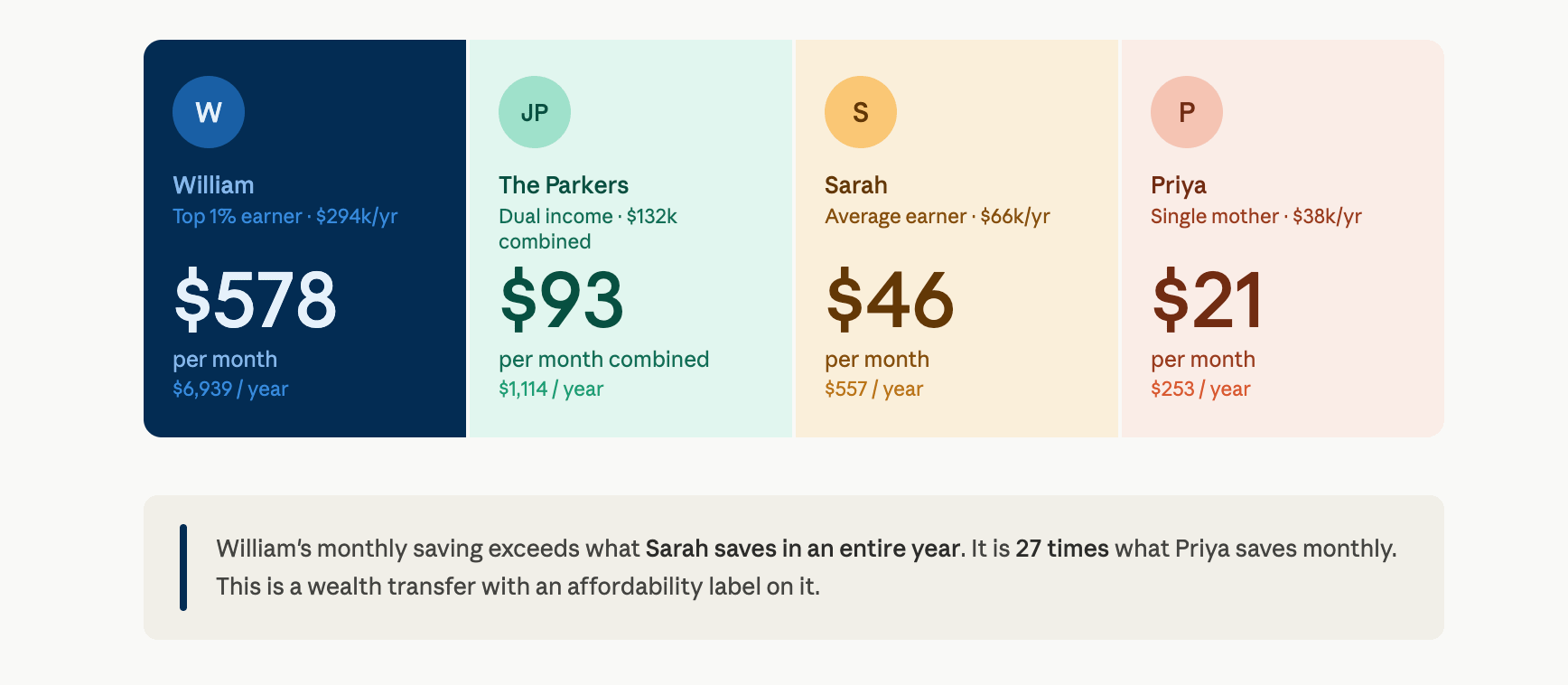

I modelled four typical British Columbian taxpayers.

William is a single professional in Vancouver earning $294,000 — the approximate threshold to be in the top one percent of BC earners. Under current rates, his annual provincial income tax bill is roughly $34,700. Under Black’s plan, it drops to around $27,800. William saves $6,939 a year. That is $578 a month.

The Parkers are a dual-income family living in Kamloops earning the BC average of $66,000 each, $132,000 combined. Each earner saves about $557 annually. Combined, the Parkers pocket an extra $1,114 a year — $93 a month between two people.

Sarah is a single average income earner making $66,000 in Kelowna. Her saving is $557 a year. Forty-six dollars a month. Just over ten dollars a week.

Priya is a single mother working in Victoria and earning $38,000, below the low income threshold for a family of two. Her saving under Black’s plan is $253 a year. Twenty-one dollars a month.

William’s monthly windfall exceeds what Sarah saves in an entire year. It is 27 times what Priya saves in a month. The $136 million in additional debt interest BC would pay annually just to borrow the revenue lost to this cut while we wait for the anticipated growth to kick in (at a conservative four percent on new bond issuance) would permanently fund approximately 600 nurses at BC median nursing salaries. Instead it purchases nothing but a substantially larger monthly cheque for William and modest, near inconsequential, saving for everyone else.

This is not affordability relief. The affordability problem in BC is not that Priya’s provincial income tax rate is too high. It is that her rent is over $2,049 a month, that BC has the highest poverty rate of any province in Canada at 13 percent, that 25 percent of BC households spend more than 30 percent of their income on housing. Twenty-one dollars a month does not move any of those numbers. It barely covers half a bag of groceries.

Black says the real payoff is investment and growth. He says lower taxes attracts high-skilled workers, draws businesses, expands the economy, and ultimately revenues recover. He points to 2001 as the evidence.

This is where I want to spend some time, because 2001 is a very specific historical moment and Black is directly asking you to treat it as a general proof of a universal principle.

Gordon Campbell, as a BC Liberal premier, cut personal income tax rates by 25 percent on average in his first days in office in 2001. The BC economy subsequently grew. The Fraser Institute calls it a blueprint. Campbell’s own chief of staff, Martyn Brown, is a believer to this day. But when Brown was asked directly about the measurable impact of those cuts, he acknowledged that having the lowest personal income tax in Canada gave BC a competitive edge saying, “although it is tough to quantify its positive economic impacts.” That is Campbell’s own chief of staff. The man in the room when the decision was made can’t quantify the economic impact.

And here is what the BC Business Council — not a left-wing organization — concluded when it analyzed the period of growth that followed. Its report, examining the difference between the stagnant 1990s and the Campbell-era expansion, makes no mention of taxation as a driver. It states instead that for BC, a small open economy, “external circumstances such as commodity prices, strength of the U.S. and Asian economies, interest rates, economic conditions in other parts of this country are important factors in B.C.’s economic performance.”

External circumstances. Not the income tax rate on a marketing manager in Kelowna.

Because here is what was actually happening in 2001 and the years that followed. A two-decade decline in global commodity prices ended suddenly that year, and demand for energy, base metals, and natural resources shot upward. The Bank of Canada’s overnight rate fell to generational lows — touching 2.75 percent by 2003 — making borrowing cheap, consumer spending easy, and housing investment boom. Canadian real estate entered the long structural expansion that would eventually see prices in some cities rise by 337 percent over two decades, generating billions in property transfer tax and economic activity entirely disconnected from personal income tax rates. Housing starts in BC grew 21 percent in 2003 and 25.8 percent in 2004. None of that was caused by the rate on the second income tax bracket.

When analysts looked at what BC’s Consolidated Revenue Fund — the province’s core government account — actually collected through the Campbell years, it declined as a share of GDP. The growth in government revenue came from natural resources, real estate transaction taxes, and the commodity super-cycle. Not from income tax receipts expanding as a result of supply-side stimulus.

Today’s conditions are the inverse of everything that made the post-2001 period work. Interest rates are elevated after the fastest monetary tightening cycle in modern Canadian history. There is no commodity super-cycle. The housing market is in a structural affordability crisis that suppresses consumer spending rather than generating windfall revenues. BC’s largest trading partner is in active tariff conflict with Canada. The conditions that happened to coincide with Campbell’s cuts do not exist.

And the research on whether personal income tax cuts specifically drive business investment is weaker than Black’s pitch requires. The evidence that corporate tax cuts stimulate business investment is reasonably solid. Personal income tax cuts are different. An NBER study found their effects on GDP are short-lived and statistically insignificant beyond three years. And the clearest statement on whether tax incentives drive business decisions came not from a left-wing critic but from Paul O’Neill, chairman and CEO of Alcoa, and George W. Bush’s own Treasury Secretary. Testifying at his Senate confirmation hearing, O’Neill said: “If you are giving money away I will take it. If you want to give me inducements for something I am going to do anyway, I will take it. But good business people do not do things because of inducements.”

That is a Republican Treasury Secretary, a lifelong corporate executive, saying plainly that tax incentives do not drive serious business location decisions. Demand does. Infrastructure does. Regulatory certainty does. A skilled workforce does. Not whether a real estate developer in Burnaby pays 16.8 percent or 13.4 percent on the portion of her income above $186,000.

Now look at the hole this cut leaves and what it actually compares to in human terms.

K-12 operating grants to all 60 of BC’s school districts total $7.3 billion for 2025-26. Black’s revenue cut is nearly half that entire budget, eliminated permanently from the treasury before a single efficiency saving has been identified or delivered. The child welfare budget stands at $4.3 billion — already exceeded by what BC pays in annual debt interest. The social services sector in total runs to $10.9 billion per year. Black is proposing to cut revenue equal to 31 percent of that entire sector on a promise that growth will eventually compensate, backed by a historical example that was driven by a commodity boom he cannot conjure.

And about those efficiency savings. Black says he can find three percent of government revenue in waste reduction; approximately $2.5 billion. But the cut he is proposing removes $3.4 billion from personal income tax revenue alone. His efficiency savings do not cover his own tax cut by nearly a billion dollars and that is before a single dollar of the existing $9.6 billion deficit is addressed. He cannot make his own numbers work on the most generous possible reading of them.

I have a simple question and I do not think it has been asked clearly enough.

If Black is confident enough in that $2.5 billion to make it a public commitment, why is his first act not to apply those savings to the $9.6 billion deficit and begin reducing a debt load that is already costing BC $4.4 billion per year in interest? Why does the money flow immediately to a tax cut that delivers $578 a month to William and $21 a month to Priya, while the debt that is eating the public balance sheet continues to compound?

A genuine fiscal conservative pays the debt down first and stabilizes the fiscal institution before making new spending promises. Acknowledges that a province running a deficit approaching $10 billion is not in a position to volunteer away revenue on the theory that growth will eventually compensate. That is not timidity. That is what conservatism actually means when it is operating in good faith.

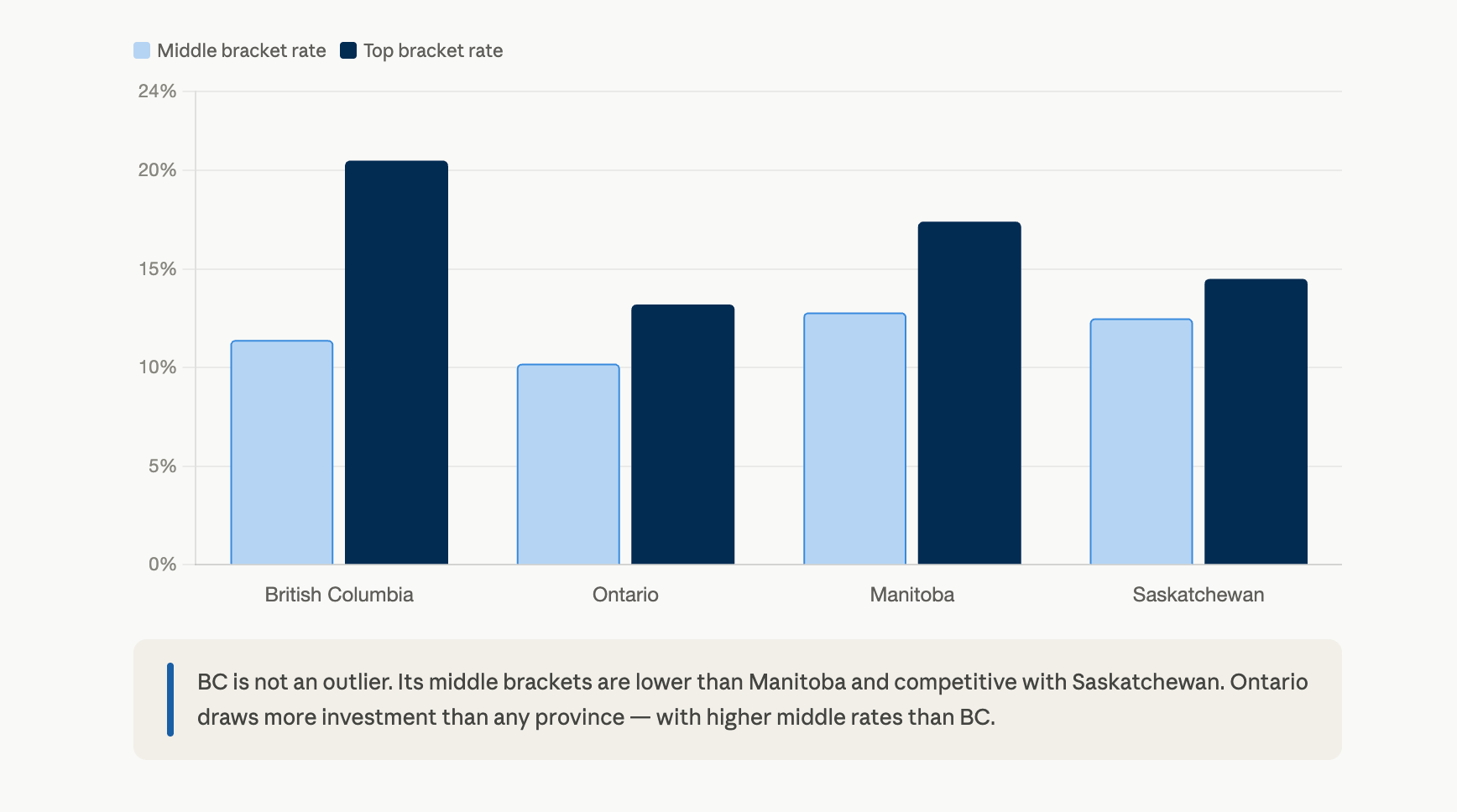

Consider the provincial comparison Black’s argument requires you to ignore. Ontario’s provincial income tax runs from 5.05 percent at the bottom to 13.16 percent at the top. Manitoba charges 10.8 to 17.4 percent. Saskatchewan runs 10.5 to 14.5 percent. In the middle brackets — income between $100,000 and $140,000 — BC charges between 10.5 and 12.29 percent. Ontario charges 9.15 to 11.16 percent in the same range. The premise that BC’s tax burden in these brackets is chasing away investment runs directly into the fact that those brackets are already lower than Manitoba, competitive with Saskatchewan, and only modestly higher than Ontario; where investment flows regardless. BC had real economic growth in 2022 and 2023 with these exact rate structures in place. The problem is not the rate. The problem is global interest rates, housing costs, tariff uncertainty, and commodity prices. None of which a provincial income tax cut addresses.

And yet Black’s plan cuts those brackets too, at full cost to the treasury, on top of everything else.

I want to end on something that troubles me more than the specific numbers do, because the numbers are bad enough on their own.

Iain Black is running as a conservative. He spent three years on BC’s Treasury Board. He knows these numbers. He knows what $3.4 billion means against a $9.6 billion deficit. He knows that the 2001 comparison requires you to pretend that a global commodity super-cycle, generationally low interest rates, and a two-decade real estate boom were caused by the provincial income tax rate. He knows that Paul O’Neill exists, that the NBER exists, that BC’s debt service trajectory exists. He is not uninformed. He is making a choice about what to tell people.

The choice he is making is to lead with the policy that helps William the most, dress it in the language of affordability and freedom, and trust that Priya will not run the numbers. To point to 2001 and hope that nobody checks what commodity prices were doing. To package it as basic economics and bet that the word basic does the work that the evidence does not.

If I can find these gaps sitting at a kitchen table with public documents and a search engine, what happens when Black is standing at a podium in a provincial election campaign and a trained economist gets ninety seconds with the numbers? The answer is not good for Black’s fiscal credibility. The answer is the kind of thing that ends conservative campaigns and solidifies another BC NDP term.

What Black is proposing is not a plan for British Columbia. It is a tax cut for the province’s highest earners, financed by borrowed money, justified by a historical analogy that does not survive scrutiny, at a moment when BC cannot afford to be giving anything away. The people who need help most — Priya, the 253,000 on income and disability assistance, the BC households spending a third of their income on rent, the patients waiting for a nurse who isn’t there because we borrowed instead of hiring — they are not the beneficiaries of this plan. They are the ones who will absorb the consequences of it.

At the end of the day, I am just a humble front-line worker whose politics happens to be as blue as my collar. I did this math at my kitchen table. If I can see it, so can he. The question isn't whether Iain Black understands what this plan does. The question is whether he thinks you do. But if you’re anything like me, you know that not making ends meet isn’t the time to start cutting shifts and relinquishing overtime.